According to the National Institute on Retirement Security, the general advice is to save from 15% to 20% of income for retirement. However, 95% of Millenials are expected to hit retirement without enough money to maintain their living standards to the end of their lives. This fact can be partly explained by the fact that individuals with student loans have fewer retirement savings than those without student debt. However, 64% of parents are either saving or planning for college.

Thus, saving for any purpose is an integral part of budgeting and, though maybe seem too evident and ubiquitous, saving advice is never too late to be pronounced one more time.

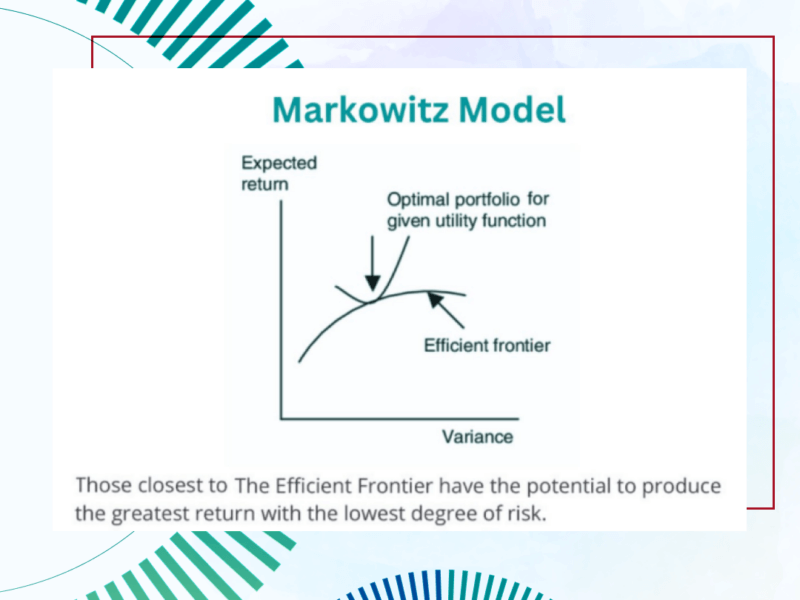

1. Money in any saving plan is not guaranteed to rise.

A saving plan performance depends on the person’s investment selection along with market conditions. Investments are subject to fluctuations. Besides, the purchasing power also goes down throughout the time amid inflation. To overcome these burdens, it is advisable to start saving as early as possible, to diversify the portfolio according to risk and time preferences and enjoy the advantage of potential compounding growth over a more extended period.

2. Adjusting asset allocation

It is the inherent part of balancing savings according to a person’s goals, age, and income. At the beginning of creating a portfolio, a person usually includes risker assets. The closer the date of saving goal (college enrollment or retirement) is approaching, the more risk-averse portfolio should become. Besides, the greater a person earns, the greater amount of money can be contributed to savings.

3. Following a contribution plan and managing withdrawals

No doubt, it’s vital in achieving saving goals. Skipping contributions or withdrawing from the account for other purposes will lead to unbalanced financial behaviour in other months. A person forced to save more to add funds by cutting costs or working more will feel frustrated and more willing to quit savings. Starting to save in advance is good from any point of view.

According to ISEC WM experience, the third point can damage your portfolio significantly if violated, while it’s the easiest part of an investment plan. It’s something that you can handle and can be controlled in most cases.

Source: nirsonline.org

Risk Warning: The information in this article is presented for general information and shall be treated as a marketing communication only. This analysis is not a recommendation to sell or buy any instrument. Investing in financial instruments involves a high degree of risk and may not be suitable for all investors. Trading in financial instruments can result in both an increase and a decrease in capital. Please refer to our Risk Disclosure available on our web site for further information.